It was a big week for spending. The consumer bought huge amounts of holiday gifts. (For my fellow Michiganders, the consumer did get much on sale because they require big savings.) The government bought a big positive revised GDP print. And Sheldon Adelson’s widow, Miriam, bought most of a basketball team. If you don’t want to feel left out, you’re welcome to read this version of the 5 Things with your credit card in hand. We’ll even offer a free year of DKI premium to anyone buying a sports team before the end of the year.

This week, we’ll address the following topics:

-

Holiday sales up big. Consumer rejects recession forecasts.

-

Market pundits have been predicting a coming recession for the last year and a half. Why hasn’t it happened? We explain.

-

GDP: More government statistics that are lies.

-

Personal Consumption Expenditures (PCE) down. Is inflation over?

-

Miriam Adelson sells $2B of $LVS stock to buy a stake in the Dallas Mavericks.

Ready for a new week of excess government and consumer spending? Let’s dive in:

-

The American Consumer Rejects a Recession:

Last Thursday marked the start of the holiday shopping season, and the American consumer showed up with enthusiasm. Online sales for the 5 days through Cyber Monday were up 8%. Online sales on Cyber Monday were up 10%. Of greater surprise, in-store retail traffic was up 2% over the weekend. While online continues to take share from bricks and mortar retail, people are still showing up to shop in person. We’re all reading about how stretched the average consumer budget is, but it’s not enough to stop people from holiday spending.

It wasn’t this bad, but people did go to the mall. Photo from thehut.com.

DKI Takeaway: Part of the increase is due to inflation, but there’s something else going on as well. Like all of you, we’ve read about increasing credit utilization and higher delinquencies. Right now, it looks like people are going to spend themselves into bankruptcy. I wouldn't be surprised to see the government backstop losses to the banks which in this specific case, could be interpreted as a bailout of the consumer. Finally, this is an election year so we will not see any fiscal discipline out of Washington any time soon. The contra-thesis is with unemployment low, government entitlement spending high, and wages rising, the consumer can handle more debt; at least for a while.

-

Where’s Our Recession?!:

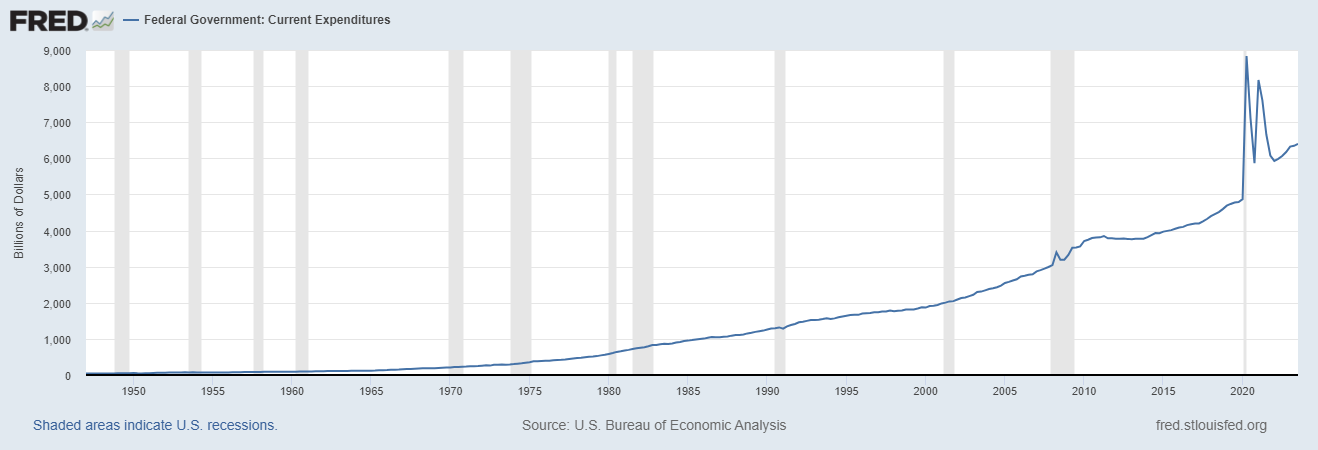

For the last year and a half, market pundits have been predicting a recession in the next quarter or two. DKI correctly predicted last year’s two quarters of negative GDP growth. It was a recession even if the government refused to acknowledge it. However, I admit that at the time, I thought the situation would be worse. Why is reality “better” than expectations?

That amount of government spending adds to GDP whether it creates value or not. Graph from St. Louis Fed.

DKI Takeaway: A few obvious culprits are higher wages and continued low unemployment. Higher interest rates are making mortgages and car financing more expensive; but also, increasing income for savers. Plus, DKI has long pointed out that most government data is manipulated to the point of being useless. DKI believes the key issue is the government is spending like we’re in a recession. This excess government spending adds to GDP even if it doesn’t create value. I don’t think the real economy is growing 5% right now, but when Congress spends like they do in the graph above, nominal (official) GDP will continue to rise.

-

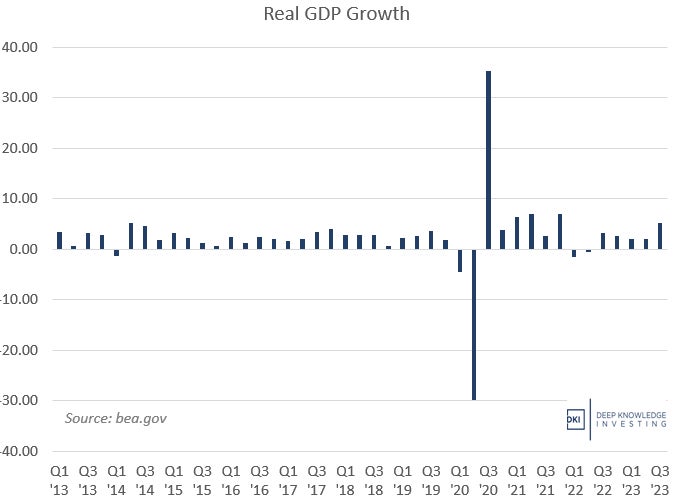

GDP Revised Upwards:

3Q GDP growth was revised upwards from 4.9% to 5.2%. As we’ve pointed out multiple times in this week’s 5 Things, government statistics are heavily manipulated. GDP is skewed by massive government overspending. For those hoping for the realization of the “soft landing” scenario, the revision was welcome news. While higher GDP would give the Federal Reserve a reason to stay “higher for longer” reduced headline inflation numbers have given the market appropriate hope that the Fed is done hiking this cycle.

It's impossible to tell how much of this growth is due to high employment and a strong work ethic and how much is due to excess government spending.

DKI Takeaway: Government numbers are always manipulated, inaccurate, and highly subject to revision. However, for most of 2023, the revisions have been so large that many investors are beginning to ignore reported economic data altogether. After all, why make a decision based on “data” that will be changed in a few weeks. One thing that makes this particular revision interesting is the direction. The most common pattern is the government reports excellent results when everyone is watching, and then revises the numbers in a more negative direction a month or two later when they’ll receive less attention. This week’s revision reversed that pattern with the revision showing a “better” result.

-

PCE Declines Further:

While the market tends to focus on the consumer price index (CPI), the preferred inflation index of the Federal Reserve is the Personal Consumption Expenditures Index (PCE). The October PCE was up 3.0% and the core number which excludes food and energy was up 3.5%. Both of these numbers are still too high, but are coming down as seen in the below chart. These figures were also consistent with market expectations. Typical for recent results, services pricing was above pricing for goods.

DKI was early and right in warning about inflation. We acknowledge that this month shows improvement.

DKI Takeaway: Many market observers are declaring this the end of inflation and continuing the call for a return to lower interest rates. I have a different view. Fed Chairman, Powell, has correctly said that changes in interest rates have a variable effect on a lag. That means that raising or lowering rates will change future inflation by an unknown amount at an uncertain time. There’s no question that Fed rate hikes are helping bring down inflation (along with annualizing the massive 2022 inflation numbers). However, Congressional overspending is causing the Treasury to issue trillions of dollars of currency to monetize our ever-growing debt. This is like filling a bathtub with the drain open and wondering if you’ll ever empty or overfill the tub. What do you think: Should the Fed keep rates where they are or start to reduce?

-

Non-Casino Exec Sells Gaming Stock to Buy a Non-Controlling Stake in the Mavericks:

Sheldon Adelson, the former CEO and Chairman of Las Vegas Sands LVS, owned a little over 50% of Sands’ stock. Advisors asked him to reduce his stake to increase the float of publicly traded shares and to reduce the potential overhang of a future sale. Adelson always saw more value in the stock and refused. When he died a few years ago, his shares passed on to his widow, Miriam. This week, she agreed to sell $2B of $LVS stock to buy a stake in the Dallas Mavericks. She will not take over management of the basketball team.

Mark Cuban, Miriam Adelson, Sheldon Adelson. Photo from reviewjournal.com.

DKI Takeaway: Miriam Adelson is a physician and a philanthropist. She is not a gaming executive and has never held an operating role in a gaming company. While the sale caused $LVS stock to decline temporarily, reducing the overhang of her massive stock ownership is good for the company. Sands is continuing to recover quickly back to pre-pandemic operating levels, and the company bought back $250MM of Mrs. Adelson’s stock at a discount. The decline in the stock this week should be temporary. While this piece was in edit, Inside Asian Gaming reported that Macau Gross Gaming Revenue (GGR) was up 435% vs last year and that mass gaming revenues are already exceeding 2019 pre-pandemic levels. Fundamentals at $LVS are excellent.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.