(Monday market open) Given how the markets hang on every word spoken publicly by Federal Reserve Chair Jerome Powell, it only seems like he’s always speaking from a mountain top. This week, he will come close to making that metaphor literal.

Powell’s speech on Friday morning at the Jackson Hole Economic Policy Symposium near the Tetons looms as arguably the most anticipated market-related event this week. Investors roughed up by the market’s August nosedive are sure to have ears up for any clues as to the Fed’s next moves.

Powell may be under pressure to demonstrate the central bank’s inflation-fighting resolve, especially after a string of stronger-than-expected data that suggest the U.S. economy continues to chug along, even with the Fed having hiked benchmark short-term rates to 22-year highs.

U.S. stocks are poised for a slightly firmer open, with futures based on the S&P 500® index (SPX) up around 0.5% near the end of overnight trading. U.S. stocks are coming off three consecutive down weeks as rising Treasury yields, signs of trouble in China’s economy, and uncertainty over Fed policy weighed on the market. The 10-year Treasury yield is starting the week around 4.30%, near a 16-year high.

Morning rush

- The 10-year Treasury note yield (TNX) rose about 5 basis points at 4.302%.

- The U.S. Dollar Index ($DXY) dipped to 103.28.

- Cboe Volatility Index®(VIX) futures were down 0.45 at 18.05.

- WTI Crude Oil futures (/CL) increased 97 cents to $81.63 per barrel.

Eye on the Fed

In late July, the Fed raised its funds rate to a target range of 5.25% to 5.50%, the 11th increase since March 2022. Investors appear confident the Fed will keep rates unchanged at its September policy meeting. The outlook after that has grown murkier, and minutes released last week from the Fed’s July 25–26 policy meeting showed that central bank leaders remained concerned over inflation and a tight labor market.

As a result, Wall Street has grown less certain the Fed is done raising rates. Inflation has steadily declined in recent months but remains above the Fed’s 2% long-term target.

Early Monday, odds that the Federal Open Market Committee (FOMC), the Fed’s policy-setting arm, will hold rates unchanged in September stood at 89%, according to the CME FedWatch Tool. For the following FOMC meeting in November, expectations rates would remain at the 5.25% to 5.50% range were about 63%.

Stocks in spotlight

The bulk of earnings season has passed, but there are still some 259 companies expected to report quarterly results this week.

- Technology shares may receive an early boost from Palo Alto Networks PANW, which late Friday reported quarterly results that surpassed analysts’ expectations. The cybersecurity company posted earnings per share of $1.44 in the previous quarter, up from 80 cents for the same quarter a year earlier and about 16 cents above expectations.

- Company earnings are expected from a variety of sectors, including Dick’s Sporting Goods DKS, Medtronic MDT, Lowe’s LOW, Macy’s M, Nvidia NVDA Toll Brothers TOL, and Zoom Video Communications ZM. Zoom is expected to report results after Monday’s close. Once a high-flier during the pandemic, Zoom shares started a sharp descent about two years ago and have remained largely earth-bound ever since. Zoom shares ended last week at $66.29, down 1.5% for the year and far below a peak near $589 in October 2020.

- Lowe’s numbers are sure to draw keen investor interest in the wake of Home Depot HD results last week that indicated consumer caution on big-ticket purchases. Medtronic will offer a glimpse of the market for medical devices after the health care sector sagged this summer. Toll Brothers may provide insights into the luxury home market and could draw further scrutiny after Warren Buffett’s Berkshire Hathaway (NYSE: BRK-A) bought shares of several home-building companies recently.

Some short-term market indicators suggest equity prices may be due for a rebound after slipping much of this month, says Randy Frederick, managing director of trading and derivatives at the Schwab Center for Financial Research. Equity volume ratios for put and call options, for example, have reached a “bearish extreme,” which is actually a bullish signal indicating stock prices may be oversold. Read more of Randy’s insights in his Weekly Trader’s Outlook.

What to watch

This week’s economic calendar is relatively light, though investors will receive some updates on consumer sentiment and the housing industry.

Scheduled reports include July Existing Home Sales on Tuesday and New Home Sales on Wednesday.

Existing home sales are expected to come in at an annual rate of 4.15 million, based on a Briefing.com consensus forecast—down slightly from 4.16 million in June. New home sales in July totaled 705,000, according to Briefing.com, which would be up from a seasonally adjusted annual rate of 697,000 in June.

Other economic releases this week include Durable Goods Orders from the Census Bureau on Thursday and the August University of Michigan Consumer Sentiment numbers on Friday. Key reports next week include Personal Consumption Expenditure (PCE) prices and Gross Domestic Product (GDP) updates.

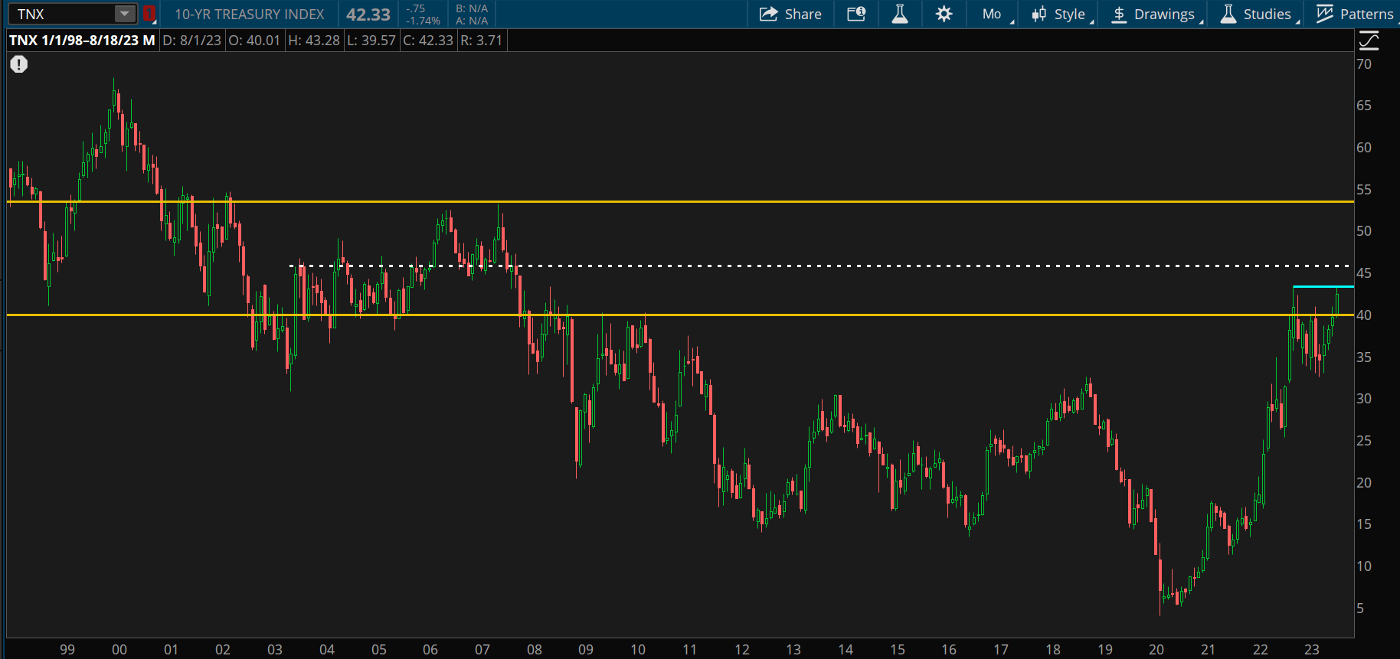

CHART OF THE DAY: YIELD WATCH. The 10-year Treasury yield (TNX) closed above a long-term resistance level last week, surpassing 4.0%, which may have technical analysts looking for a potential rally to another historical resistance level around 5.35%. Looking at the 25-year monthly chart, the 4.575% level could also be a potential congestion point. Rising yields can hurt current bondholders because of the inverse relationship between yield and bond prices. Additionally, the 10-year yield also tends to correlate with the 30-year mortgage, so housing stocks are likely to struggle if this breakout follows through. Data sources: S&P Dow Jones Indices, Cboe. Chart source: thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Thinking cap

Ideas to mull as you trade or invest

Plastic gets pricey: Americans’ habit of carrying balances on their credit cards is getting increasingly costly. The average credit card interest rate is now slightly over 21%, according to Bankrate.com. That’s more than three points higher than the pre-pandemic record set in July 2019 and nearly five points higher than the average card annual percentage rate (APR) in March 2021. Rising credit card rates are a direct result of the Fed’s efforts to tame inflation. The central bank last month hiked its benchmark funds rate to its highest point in over 22 years. Many credit card rates are based on the prime rate, which is also controlled by the Fed and moves in lockstep with the fed funds rate. The prime rate, which is typically about 3 percentage points above the funds rate, is what banks often charge their best customers. “With the U.S. prime rate at its highest point in decades, credit card lenders are rapidly adjusting the offers they advertise online and pushing up starting APR to record heights,” Bankrate says in a report. “As a result, consumers on the hunt for a brand-new card are finding it all-but-impossible to secure a rate that’s anywhere close to what they could get a few years ago.”

Goldman sanguine on corporate debt outlook; others beg to differ: Rising U.S. interest rates are generating concern over expanding levels of distressed debt, and possibly even a wave of defaults across parts of the corporate credit market. In a report, Goldman Sachs Chief Credit Strategist Lotfi Karoui said he’s generally optimistic over the U.S. corporate credit outlook, saying healthy fundamentals should allow most companies to weather a challenging borrowing environment. “The risk of a full-blown default cycle is still fairly low, at least if we’re talking about the next 12 months,” he says. “I would characterize things as ‘mean reversion’ without a severe deterioration.” Not everyone agrees. Boaz Weinstein, chief investment officer of Saba Capital Management, notes that credit spreads are currently at the lower end of the post-global financial crisis range and “aren’t sufficiently pricing in the present high level of macroeconomic uncertainty,” according to the Goldman report. Corporate defaults “will almost certainly rise from here,” Weinstein adds.

Buck up before you fuel up: Filling up your tank for a Labor Day weekend road trip likely will set you back a little more than what you paid earlier this summer. WTI crude oil futures, the U.S. benchmark, have rallied as much as 23% since dipping under $70 per barrel in late June and on August 20 reached a nine-month high near $85. Extended gains or declines in oil prices typically take two to four weeks to filter down to the pump, which means it’s likely retail fuel has further upside over the next few weeks. Pump gasoline has already been climbing. Late last week, regular-grade gasoline averaged $3.873 a gallon nationwide, up nearly 9% from a month earlier, according to AAA. Some relief may be in sight for motorists. Gasoline futures, which reflect wholesale prices, ended last week around $2.59 in the October contract, down about 22 cents from the September contract.

Calendar

Aug. 22: July Existing Home Sales and expected earnings from BJ’s Wholesale Club Holdings (BJ), Dick’s Sporting Goods (DKS), Lowe’s (LOW), Macy’s (M) Medtronic (MDT) and Toll Brothers (TOL).

Aug. 23: July New Home Sales, and expected earnings from Foot Locker (FL), Kohl’s (KSS), and Nvidia (NVDA).

Aug. 24: July Durable Orders and expected earnings from Dollar Tree (DLTR) and Gap (GPS).

Aug. 25: Fed Chair Powell speaks at Jackson Hole Summit, Final August University of Michigan Consumer Sentiment.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.