Megacap tech-related stocks could end up being the story today as the broader market seems well supported but without a catalyst to make big moves higher.

The FAANG names—Facebook, Inc. FB, Apple Inc AAPL, Amazon.com, Inc. AMZN, Netflix Inc NFLX and Alphabet Inc’s GOOGL Google—seem to be in recovery mode as the yield on the 10-year Treasury remains under 1.7%.

These are trusted names that investors are tending to buy on the dips at the moment as people try to figure out where the main thrust of the market is going to go next. There’s still a valuation debate going on as investors and traders continue to evaluate the state of the economic recovery and whether they want to put more money into stay-at-home or back-to-work stocks on any given day.

The performance of growth stocks, including the FAANGs, is related to the economic recovery in part because of fears that the recovery will come with potentially problematic inflation. As inflation expectations, and the yield on the 10-year Treasury rise, growth stocks can take a hit because inflation expectations can eat away at how much people think they might be worth in the future.

So if we see the yield on the 10-year rise back above 1.7%, we might see more pressure on tech-related megacaps and other growth stocks.

Meanwhile, investors seem confident in the market given the Fed’s reiterated easy monetary policy stance and the vaccine rollout’s help for the economy.

That leaves the SPX looking for yet another record close. If it can manage that today, it would be the index’s 19th record finish this year, which is pretty amazing given that we’re just over one quarter into the year.

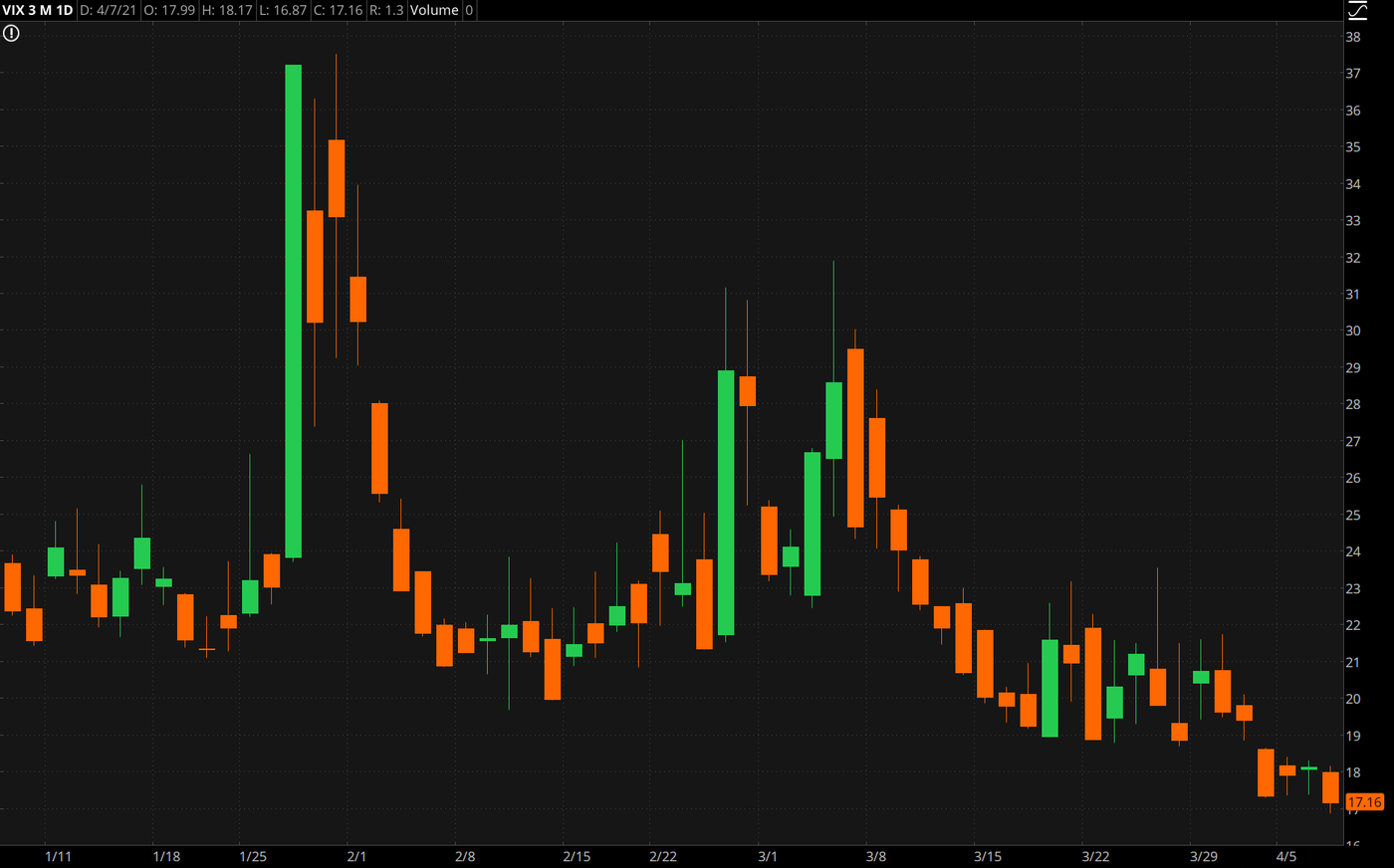

Watching Grass Grow

Some days, market activity is a bit like watching beige paint dry—just not all that interesting—relative to the action over the past year, which has, at times, been a bit too eventful. This week, trading volumes have been light, and the Cboe Volatility Index (VIX) has continued its slow march downward. VIX begins the day with a 16 handle for the first time since February 2020 (see chart below).

Sometimes that can be a good thing. With equities doing as well as they have been, a mostly-sideways day is probably healthy. The three main U.S. stock market indices ended mixed yesterday with the S&P 500 Index (SPX) and the Dow Jones Industrial Average ($DJI) showing slight gains and the Nasdaq Composite (COMP) posting a slight loss.

The lackluster trading came as the minutes from the Fed’s last policy-setting meeting weren’t surprising. Central bankers said the economy is far from maximum employment and price stability, which we already knew. Even though the last jobs report was better than expected, weekly jobless claims figures remain elevated. And inflation remains under the Fed’s 2% target.

With that backdrop, central bankers also reiterated that asset purchases—which have contributed to easy monetary policy along with the Fed’s very low policy interest rate—would continue, another thing we already knew.

So by the end of the day, the supportive news about accommodative policy and negative news about economic uncertainty appeared to be a wash with investors because those issues have already been baked into the proverbial cake.

Dimon In The Rough

The Fed wasn’t the only one providing a mixed message on Wednesday. Jamie Dimon, CEO of JPMorgan Chase, said that an economic boom could last into 2023. That’s especially encouraging coming from the head of the largest bank in the United States.

But Dimon also said that there is a possibility that a rise in inflation might not just be temporary. Such a scenario would likely erode the value of growth stocks and push investors more into cyclical stocks that would benefit from gains in the economy.

Inflation expectations have helped push longer term Treasury yields higher as vaccines open the economy, stimulus checks hit bank accounts, Washington discusses big infrastructure spending, and the Fed keeps monetary policy easy.

Some—including policymakers at the Fed—think a spike in inflation could be transitory, but another school of thought worries about it being a longer-term issue. That has already put some pressure on growth stocks, but that pressure has been easing as yields have more or less stabilized.

Still, with the 10-year edging back below 1.7%, the inflation story seems to be relegated to the back burner, while a renewed interest in big-tech gently simmers up front.

CHART OF THE DAY: CALMING NERVES. As you might expect on a day when the main three U.S. indices didn’t move all that much, Wall Street’s main fear gauge was also subdued yesterday. The Cboe Volatility Index (VIX—candlestick) has been on the decline as traders and investors get more comfortable with the economic outlook as the vaccine rollout helps open up the economy. Data source: Cboe Global Markets. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Just Passing Through: Later this week, we’ll get another look at inflation in the form of producer prices. That economic metric probably isn’t as closely scrutinized as consumer price data, but the producer price index is still important to watch. While companies that produce goods can eat some of the rising costs that come with, say, increasing commodities prices, they’re not likely to swallow them all. That means they’ll push those costs through to consumers, a phenomenon that’s already been happening in the U.S. manufacturing sector. On Friday, the March producer price index is expected to show a rise of 0.5%, according to a Briefing.com consensus. Last time around, the market news and research service said “there was a sightline to pipeline inflation pressures.”

The Chips Are Down: We’ve talked about the global microprocessor shortage before, as it’s been an Achilles heel for automotive companies just at a time when demand is ramping up. Government data on Wednesday underscored how the chip shortage is affecting the U.S. economy, as automotive imports dropped. Census Bureau data showed the U.S. trade deficit in February rose more than expected to hit a record $71.1 billion as exports dropped 2.6% and imports dropped 0.7%. “The key takeaway from the report is that the impact of the semiconductor shortage was apparent in the $3.4 billion decrease in imports of automotive vehicles, parts, and engines,” Briefing.com said. With the economy recovering and auto demand increasing along with it, foreign and domestic vehicle manufacturers have warned the chip shortage is holding up production.

Revolving Door: In another apparent sign that the economy is on the mend, consumer credit rose much more than expected in February, according to data released Wednesday. Total credit jumped by $27.6 billion when a Briefing.com consensus had only expected a gain of $5 billion. “The key takeaway from the report is that revolving credit expanded for only the second time in the last 12 months and was the largest increase in revolving credit since July 2019,” Briefing.com said. The consumer credit report from the Federal Reserve shines a light on how much revolving credit, such as credit cards, and non-revolving credit, such as car loans, Americans have outstanding. Increasing consumer debt can be an indicator that people are more comfortable with the economy and their job prospects and can be a boon for consumer spending that works its way into personal consumption and retail sales reports. Consumer spending makes up the largest percentage contributor to gross domestic product.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.